- Home

- Client Advantages

-

Client Successes and Placements

- Clients of the Merwin Group

- Types and Range of Grid Clients

- Grid Positions, Functions and Placements

- Grid Staffing Successes

- Record of Success – ABB Case Study

- Qualifying and Placing Utility Analytic Talent

- 3511 - Technical Project Manager

- Smart Energy - Engineering Director

- Utility Analytic Returns - Your Opportunities

- Our Qualifications

-

Our Own Grid Experience

- Merwin Group in the Grid

- Planning, Developing and Executing Projects

- Electric Utility Services

- Green Electric Power Generation, Transmission and Distribution

- Electric Peak Shaving - Transmission & Distribution - Washington, DC

- Electric Load Leveling - New York City - Brooklyn Navy Yard

- Electric Repowering -- Manchester Street Station - Providence, RI

- Electric Utility Inovations

- Power Your Smart Advantage Program

- Blogs

- Contact

- Privacy Policy

18.12.2024

Mark Reisner

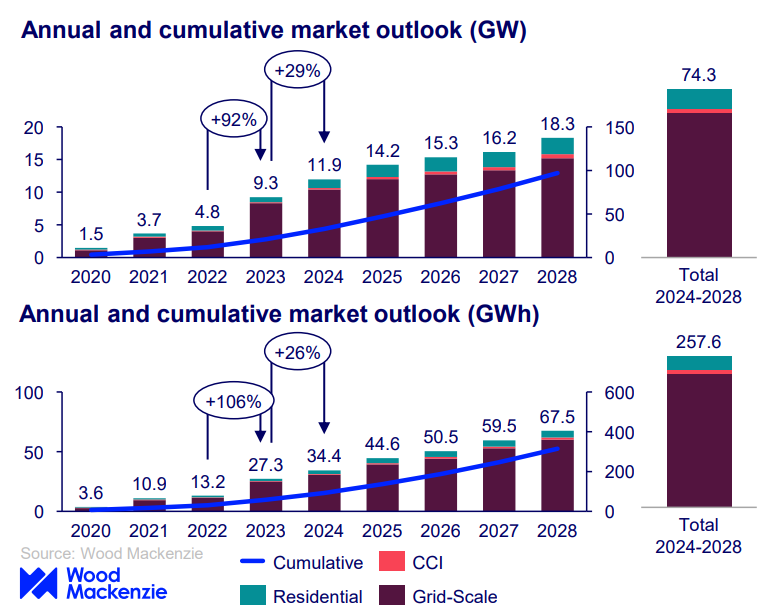

The US energy storage market recorded a new milestone in unprecedented growth in 2024, which implies maturity and vitality to the nation's transition towards a more sustainable energy future. As reported, tremendous strides have been made across all segments. In particular, there has been an emphasis on grid-scale deployments, with the recent pick-up pace being stimulated by policy incentives, technological breakthroughs, and regional leadership.

The "U.S. Energy Storage Monitor" report by Wood Mackenzie and the American Clean Power Association (ACP) reflects the energy storage industry's excellent performance. During the second quarter of 2024, the U.S. deployed 3,011 MW and 10,492 MWh, its second-best quarter ever. Notably, grid-scale storage continued to drive this growth, contributing 2,773 MW and 9,982 MWh.

The residential and community/commercial sectors also increased significantly. Year-over-year, residential storage went up 12% to 423 MWh; even so, certain regions like California and Puerto Rico face the adjustment of incentives. The community and commercial sector saw a 61% increase from year-over-year to 87 MWh, which signifies excellent momentum.

Driving Growth

The most significant transformative change for this industry has been the standalone Storage Investment Tax Credit, launched through the Inflation Reduction Act. This credit expands the economic appeal of the energy storage system, thereby increasing adoption in the utility, residential, and commercial sectors.

Regional leaders, such as California, Arizona, and Texas, have also played a dominant role, with an 85% share of the total installations made during Q2 2024. These states express successful outcomes that can be achieved whenever a given policy and its investment come at a given scale.

https://www.energy-storage.news/us-energy-storage-deployments-soar-80-to-nearly-10gwh-in-q3-2024/

Long-Term Outlook

Looking forward, the energy storage market will continue on its growth path. In 2024 alone, deployments will reach 12.8 GW and 36.9 GWh, increasing year over year by 42%. Over the next five years, cumulative deployments will hit 62 GW in the grid-scale segment, while the residential and distributed storage market will add 12 GW by 2028.

However, not all is smooth sailing; the industry faces some operational challenges. Project delays from early-stage issues, the complexity of a permitting process, and supply chain constraints are still affecting timelines. The commercial and community segment is sensitive to development complexities and limited incentives, tempering its growth prospect.

A Bright Future Ahead

Notwithstanding the challenges, the energy storage industry is likely to be one of the cornerstones of the clean energy transition in the United States. This is because sustained policy support, technological innovation, and investment mean the sector will continue meeting the growing needs of a modern and decarbonized energy grid.

Recent Posts